Do I Have to Pay Capital Gains Taxes Immediately? In most cases, you must pay the capital gains tax after you sell an asset.

What triggers capital gains tax on real estate?

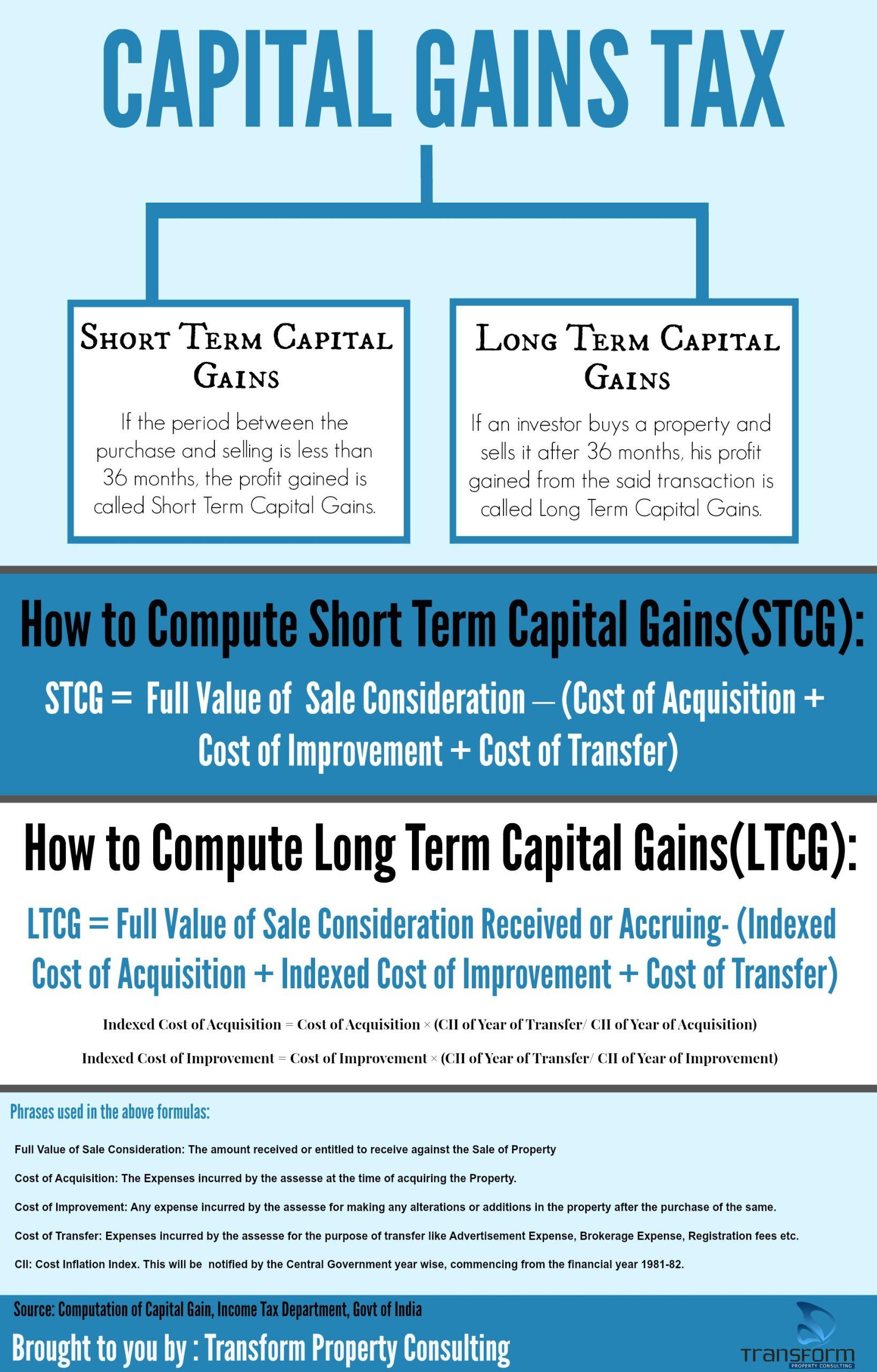

If you buy a home and a dramatic rise in value causes you to sell it a year later, you would be required to pay full capital gains tax—short-term or long-term on the house, depending on exactly how long you owned it.

How long to own a house before selling to avoid capital gains?

The 121 home sale exclusion comes with specific restrictions: Eligibility: To be eligible for the exclusion, you must have owned and used the property as your primary residence for at least 2 of the 5 years preceding the sale.

How is capital gains calculated on sale of real estate?

Subtract your basis (what you paid) from the realized amount (how much you sold it for) to determine the difference. If you sold your assets for more than you paid, you have a capital gain. If you sold your assets for less than you paid, you have a capital loss.

Is it better to pay capital gains now or later?

There are several ways you can minimize the taxes you pay on capital gains: Wait to sell assets. If you can keep an asset for more than a year before selling, this can usually result in paying a lower capital gains rate on that profit. Invest in tax-free or tax-deferred accounts.

Do I pay taxes to the IRS when I sell my house?

If you do not qualify for the exclusion or choose not to take the exclusion, you may owe tax on the gain. Your gain is usually the difference between what you paid for your home and the sale amount. Use Selling Your Home (IRS Publication 523) to: Determine if you have a gain or loss on the sale of your home.

New capital gain rules from April 1 — Cap on house sale, tax hike on market-linked debentures and more#CapitalGains #Tax #April1 https://t.co/qEJavbAZ7c

— CNBC-TV18 (@CNBCTV18Live) March 23, 2023

How can I avoid paying taxes when selling my house?

Home sales can be tax free as long as the condition of the sale meets certain criteria: The seller must have owned the home and used it as their principal residence for two out of the last five years (up to the date of closing). The two years do not have to be consecutive to qualify.

Does sale of house need to be reported to IRS?

Reporting the Sale

Report the sale or exchange of your main home on Form 8949, Sale and Other Dispositions of Capital Assets, if: You have a gain and do not qualify to exclude all of it, You have a gain and choose not to exclude it, or. You received a Form 1099-S.

How long do you have to live in a house to avoid capital gains tax IRS?

You're eligible for the exclusion if you have owned and used your home as your main home for a period aggregating at least two years out of the five years prior to its date of sale. You can meet the ownership and use tests during different 2-year periods.

Is selling a house good or bad for taxes?

If you sell a house or property in one year or less after owning it, the short-term capital gains is taxed as ordinary income, which could be as high as 37 percent. Long-term capital gains for properties you owned for over a year are taxed at 0 percent, 15 percent or 20 percent depending on your income tax bracket.

What can be used to offset capital gains?

Capital losses

Use capital losses to offset gains.

Say you own two stocks, one worth 10% more than you paid for it, while the other is worth 5% less. If you sold both stocks, the loss on the one would reduce the capital gains tax that you would owe on the other.

Do I have to buy another house to avoid capital gains?

Sale of your principal residence. We conform to the IRS rules and allow you to exclude, up to a certain amount, the gain you make on the sale of your home. You may take an exclusion if you owned and used the home for at least 2 out of 5 years. In addition, you may only have one home at a time.

How long do I have to buy another house to avoid capital gains?

Within 180 days

How Long Do I Have to Buy Another House to Avoid Capital Gains? You might be able to defer capital gains by buying another home. As long as you sell your first investment property and apply your profits to the purchase of a new investment property within 180 days, you can defer taxes.

What is the 6 year rule for capital gains tax?

Here's how it works: Taxpayers can claim a full capital gains tax exemption for their principal place of residence (PPOR). They also can claim this exemption for up to six years if they moved out of their PPOR and then rented it out.

At what age do you not pay capital gains?

For individuals over 65, capital gains tax applies at 0% for long-term gains on assets held over a year and 15% for short-term gains under a year. Despite age, the IRS determines tax based on asset sale profits, with no special breaks for those 65 and older.

What is the one time capital gains exemption?

You can sell your primary residence and avoid paying capital gains taxes on the first $250,000 of your profits if your tax-filing status is single, and up to $500,000 if married and filing jointly. The exemption is only available once every two years.

Is 250k capital gains exclusion?

Not All Gain Is Taxable

There is an exclusion on capital gains up to $250,000, or $500,000 for married taxpayers, on the gain from the sale of your main home. That exclusion is available to all qualifying taxpayers—no matter your age—who have owned and lived in their home for two of the five years before the sale.

How do I claim capital gains exclusion?

To claim the exclusion, you must meet the ownership and use tests. This means that during the 5-year period ending on the date of the sale, you must have: Owned the home for at least two years (the ownership test) Lived in the home as your main home for at least two years (the use test)

What is the 250 000 exclusion on the sale of a main home?

Here's the most important thing you need to know: To qualify for the $250,000/$500,000 home sale exclusion, you must own and occupy the home as your principal residence for at least two years before you sell it. Your home can be a house, apartment, condominium, stock-cooperative, or mobile home fixed to land.

What is the code section for exclusion of gain on sale of primary residence?

Section 121(a) generally provides, with certain limitations and exceptions, that gross income does not include gain from the sale or exchange of property if, during the 5-year period ending on the date of the sale or exchange, the taxpayer has owned and Page 8 8 used the property as the taxpayer's principal residence

What is the $250000 / $500,000 home sale exclusion for 2023?

Generally, people who qualify for the home sale capital gain exclusion can exclude: $250,000 of capital gains if single. $500,000 of capital gains if married and filing jointly.

How do you calculate gain on sale of home?

It is calculated by subtracting the asset's original cost or purchase price (the “tax basis”), plus any expenses incurred, from the final sale price. Special rates apply for long-term capital gains on assets owned for over a year.

What is the $250000 $500000 home sale exclusion?

The seller must not have sold a home in the last two years and claimed the capital gains tax exclusion. If the capital gains do not exceed the exclusion threshold ($250,000 for single people and $500,000 for married people filing jointly), the seller does not owe taxes on the sale of their house.9.

What is the average gain on the sale of a house?

According to ATTOM Data's year-end 2022 Home Sales Report, the average home seller earned real profit on their sale to the tune of $112,000, up 21% from 2021 and 78% from two years ago.

How much gain can you exclude from sale of home?

Key Takeaways. You can sell your primary residence and be exempt from capital gains taxes on the first $250,000 if you are single and $500,000 if married filing jointly.

How is capital gains calculated on sale of home?

Subtract your basis (what you paid) from the realized amount (how much you sold it for) to determine the difference. If you sold your assets for more than you paid, you have a capital gain.

Is money from sale of a house taxable income?

You are required to include any gains that result from the sale of your home in your taxable income. But if the gain is from your primary home, you may exclude up to $250,000 from your income if you're a single filer or up to $500,000 if you're a married filing jointly provided you meet certain requirements.

Do I have to report sale of home to IRS?

Report the sale or exchange of your main home on Form 8949, Sale and Other Dispositions of Capital Assets, if: You have a gain and do not qualify to exclude all of it, You have a gain and choose not to exclude it, or. You received a Form 1099-S.

Are home sale proceeds reported to IRS?

Reporting the Sale

If you receive an informational income-reporting document such as Form 1099-S, Proceeds From Real Estate Transactions, you must report the sale of the home even if the gain from the sale is excludable.

Who sends a 1099 when you sell a house?

When you sell your home, federal tax law requires lenders or real estate agents to file a Form 1099-S, Proceeds from Real Estate Transactions, with the IRS and send you a copy if you do not meet IRS requirements for excluding the taxable gain from the sale on your income tax return.

Are proceeds from the sale of a house considered earned income?

You are required to include any gains that result from the sale of your home in your taxable income. But if the gain is from your primary home, you may exclude up to $250,000 from your income if you're a single filer or up to $500,000 if you're a married filing jointly provided you meet certain requirements.

How do I report a 1099-s sale of my home?

If you checked Check here if you received a Form 1099-S, the sale of home transaction will be reported on Form 8949 Sales and Other Dispositions of Capital Assets and Schedule D Capital Gains and Losses. TaxAct will automatically adjust the loss to zero (0) using Adjustment Code "L."

What should I do with large lump sum of money after sale of house?

Depending on your financial circumstances, it might make sense to pay down debt, invest for growth, or supplement your retirement. You might also consider purchasing products to protect yourself and your loved ones, including annuities, life insurance, or long-term care coverage.