Within 180 days

How Long Do I Have to Buy Another House to Avoid Capital Gains? You might be able to defer capital gains by buying another home. As long as you sell your first investment property and apply your profits to the purchase of a new investment property within 180 days, you can defer taxes.

What is the best way to avoid capital gains tax on real estate?

Fortunately, the IRS gives homeowners and real estate investors ways to save big. You can avoid capital gains tax by buying another house and using the 121 home sale exclusion. In addition, the 1031 like-kind exchange allows investors to defer taxes.

What is the $250000 / $500,000 home sale exclusion?

What is the 6 year rule for capital gains tax?

Here's how it works: Taxpayers can claim a full capital gains tax exemption for their principal place of residence (PPOR). They also can claim this exemption for up to six years if they moved out of their PPOR and then rented it out.

What is the one time capital gains exemption?

You can sell your primary residence and avoid paying capital gains taxes on the first $250,000 of your profits if your tax-filing status is single, and up to $500,000 if married and filing jointly. The exemption is only available once every two years.

Is money from sale of a house taxable income?

It depends on how long you owned and lived in the home before the sale and how much profit you made. If you owned and lived in the place for two of the five years before the sale, then up to $250,000 of profit is tax-free. If you are married and file a joint return, the tax-free amount doubles to $500,000.

Where do I report the sale of a second home in TurboTax?

- Open your TurboTax account > Wages & Income.

- Scroll to Investment Income > Select Stocks, Mutual Funds, Bonds, Other > Start or Update.

- Select the type of sale (see image below)

- Enter the details of the property sold - Select Second Home from the dropdown continue to enter your information.

- Continue to finish your sale.

Frequently Asked Questions

Does selling a house affect your tax return?

Do I pay taxes to the IRS when I sell my house?

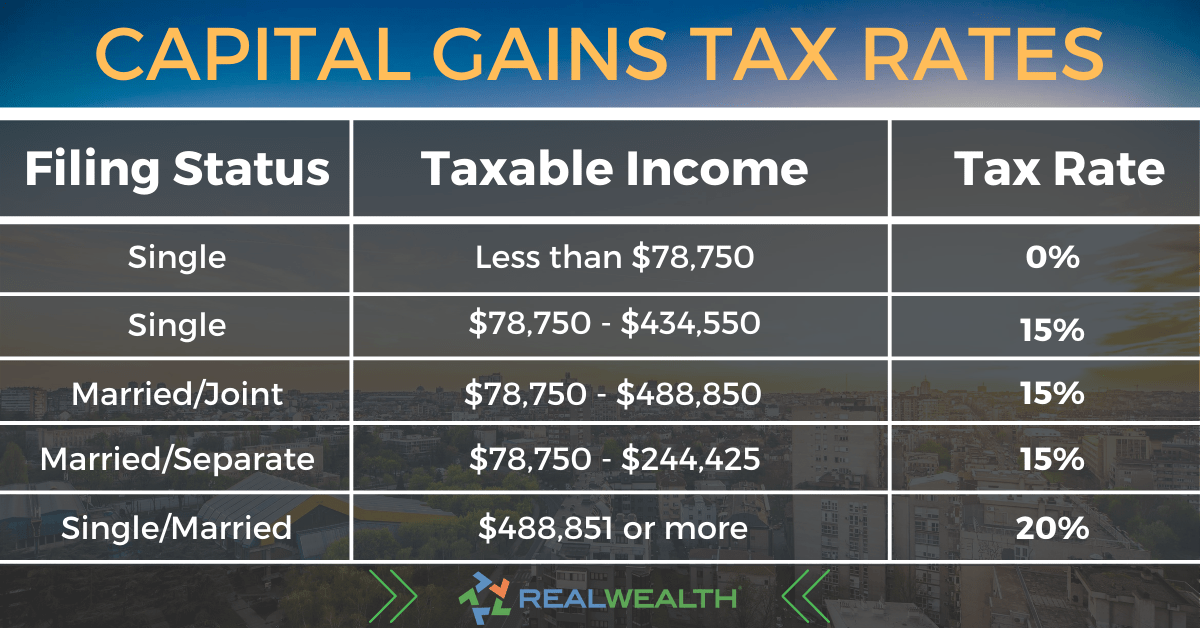

What is the capital gains tax on $200 000?

= $

| Single Taxpayer | Married Filing Jointly | Capital Gain Tax Rate |

|---|---|---|

| $0 – $44,625 | $0 – $89,250 | 0% |

| $44,626 – $200,000 | $89,251 – $250,000 | 15% |

| $200,001 – $492,300 | $250,001 – $553,850 | 15% |

| $492,301+ | $553,851+ | 20% |

Who sends 1099-s for home sale?

When you sell your home, federal tax law requires lenders or real estate agents to file a Form 1099-S, Proceeds from Real Estate Transactions, with the IRS and send you a copy if you do not meet IRS requirements for excluding the taxable gain from the sale on your income tax return.

What IRS form do I use to report the sale of real estate?

Form 1099-S

Use Form 1099-S to report the sale or exchange of real estate.

Do I have to tell the IRS I sold my house?

Report the sale or exchange of your main home on Form 8949, Sale and Other Dispositions of Capital Assets, if: You have a gain and do not qualify to exclude all of it, You have a gain and choose not to exclude it, or. You received a Form 1099-S.

Do I have to report the sale of my home to the IRS?

Report the sale or exchange of your main home on Form 8949, Sale and Other Dispositions of Capital Assets, if: You have a gain and do not qualify to exclude all of it, You have a gain and choose not to exclude it, or. You received a Form 1099-S.

Does the sale of a house count as income?

FAQ

- How do you report a sale to the IRS?

You must report the transaction (gain on sale) on Form 8949, Sales and Other Dispositions of Capital AssetsPDF, and Form 1040, U.S. Individual Income Tax Return, Schedule D, Capital Gains and LossesPDF.

- How does IRS know you sold property?

Typically, when a taxpayer sells a house (or any other piece of real property), the title company handling the closing generates a Form 1099 setting forth the sales price received for the house. The 1099 is transmitted to the IRS.

- Is there a way to avoid capital gains tax on the selling of a house?

The good news is that many people avoid paying capital gains tax on the sale of their primary home because of an IRS rule that lets you exclude a certain amount of the gain from your taxable income. Generally, people who qualify for the home sale capital gain exclusion can exclude: $250,000 of capital gains if single.

- How do you offset capital gains on a real estate sale?

Use The 1031 Exchange

The 1031 exchange strategy is a method for deferring capital gains taxes on the sale of investment real estate. It allows you to reinvest that profit into another piece of investment real estate without having to pay any capital gains tax until you sell that asset, if ever.

- How often can you exclude gain on sale of home?

Once every two years

You're only allowed to exclude gain on the sale of a home once every two years. This is true unless the reduced gain exclusion rules apply. You usually can't exclude the gain on the sale of a home if both of these apply: You sold another home at a gain within the past two years.

- Do I have to buy another house to avoid capital gains?

Sale of your principal residence. We conform to the IRS rules and allow you to exclude, up to a certain amount, the gain you make on the sale of your home. You may take an exclusion if you owned and used the home for at least 2 out of 5 years. In addition, you may only have one home at a time.

- Do you pay capital gains immediately or at tax time?

In most cases, you must pay the capital gains tax after you sell an asset. It may become fully due in the subsequent year tax return. For example, selling a security in 2021 that is subject to capital gains taxes may result in taxes due for your annual tax return filing for 2021 that is due in the spring of 2022.

- Are capital gains taxes taken out at closing?

- You only pay the capital gains tax after you sell an asset. Let's say you bought your home 2 years ago and it's increased in value by $10,000. You don't need to pay the tax until you sell the home.

How many times in a tear can capital gains tax of real estate be claimed

| Is capital gains before or after closing costs? | Because capital gains can only be assessed when an investment is sold, you pay this tax when selling property to another party. It's not part of your monthly mortgage payments like property tax. And even though it's applicable when selling a home, you don't pay this tax as part of your closing costs. |

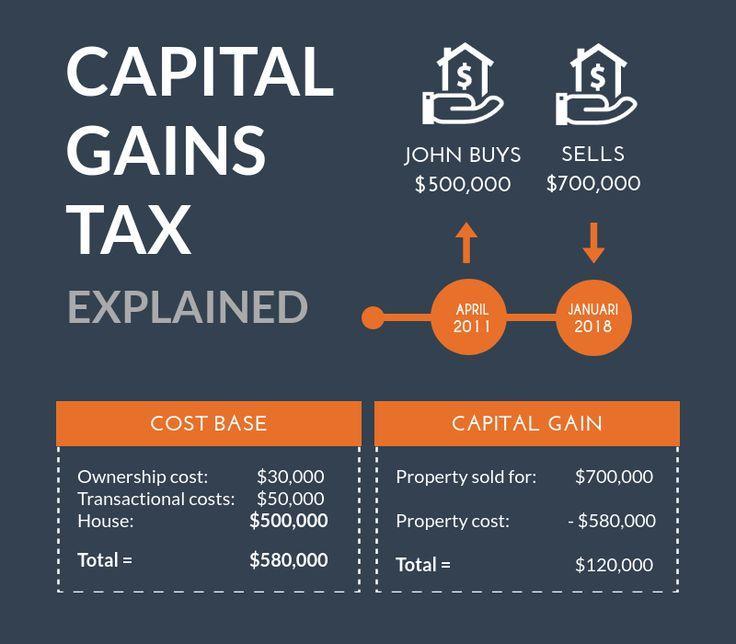

| How do you calculate capital gains tax on the sale of a home? | Capital gain calculation in four steps

|

| Do I need to make an estimated tax payment for capital gains? | If the amount of income tax withheld from your salary or pension is not enough, or if you receive income such as interest, dividends, alimony, self-employment income, capital gains, prizes and awards, you may have to make estimated tax payments. |

| Is profit from the sale of your home taxable income? | It depends on how long you owned and lived in the home before the sale and how much profit you made. If you owned and lived in the place for two of the five years before the sale, then up to $250,000 of profit is tax-free. If you are married and file a joint return, the tax-free amount doubles to $500,000. |

| What is the exclusion of gain on the sale of a home? | If you have a capital gain from the sale of your main home, you may qualify to exclude up to $250,000 of that gain from your income, or up to $500,000 of that gain if you file a joint return with your spouse. |

| How long to own a house before selling to avoid capital gains? | The 121 home sale exclusion comes with specific restrictions: Eligibility: To be eligible for the exclusion, you must have owned and used the property as your primary residence for at least 2 of the 5 years preceding the sale. |

| What are exceptions to the 2 year capital gains rule? | Exceptions to the 2-out-of-5-Year Rule You might be able to exclude at least a portion of your gain if you lived in your home less than 24 months but you qualify for one of a handful of special circumstances such as a change in workplace, a health-related move, or an unforeseeable event. |

| How do you avoid capital gains tax on property? | A few options to legally avoid paying capital gains tax on investment property include buying your property with a retirement account, converting the property from an investment property to a primary residence, utilizing tax harvesting, and using Section 1031 of the IRS code for deferring taxes. |

- How many times can I claim capital gains exemption?

Once every two years

You can sell your primary residence and avoid paying capital gains taxes on the first $250,000 of your profits if your tax-filing status is single, and up to $500,000 if married and filing jointly. The exemption is only available once every two years.

- Can capital gains be taxed twice?

But are those capital gains taxed twice? It depends. When it comes to traditional asset investments (such as stocks), proceeds from the sale can be taxed twice, once at the corporate level and again at the personal level. Then there are capital gains at the state level.

- What is the statute of limitations on capital gains tax returns?

The important and increasingly controversial exception to the normal three-year rule is that in some circumstances, the limitations period is extended to six years. A lot can happen in three years, so you'll want to know whether your return is hot for three years or six.

- How do I avoid paying capital gains tax on real estate?

A few options to legally avoid paying capital gains tax on investment property include buying your property with a retirement account, converting the property from an investment property to a primary residence, utilizing tax harvesting, and using Section 1031 of the IRS code for deferring taxes.

- Can I claim more than $3000 capital gain or loss?

Your maximum net capital loss in any tax year is $3,000. The IRS limits your net loss to $3,000 (for individuals and married filing jointly) or $1,500 (for married filing separately). Any unused capital losses are rolled over to future years. If you exceed the $3,000 threshold for a given year, don't worry.

- What should I do with large lump sum of money after sale of house?

Depending on your financial circumstances, it might make sense to pay down debt, invest for growth, or supplement your retirement. You might also consider purchasing products to protect yourself and your loved ones, including annuities, life insurance, or long-term care coverage.

- Do you pay short term capital gains if you reinvest?

- Yes, you will have to pay tax on stock gains even if you reinvest. However, how much you will have to pay can vary, depending on how long you've held the stock, and your income level. You can also participate in tax-loss harvesting by selling other stocks in your portfolio at a loss to offset your total tax burden.

- How long do I have to buy another home to avoid capital gains?

Within 180 days

How Long Do I Have to Buy Another House to Avoid Capital Gains? You might be able to defer capital gains by buying another home. As long as you sell your first investment property and apply your profits to the purchase of a new investment property within 180 days, you can defer taxes.