5 days ago

Basically, if you sell a property within 36 months of buying it, you might have to pay CGT. The main goal of this rule is to stop people from avoiding taxes by quickly buying and selling properties. However, there are some special cases where this rule doesn't apply.

Do I have to pay capital gains tax immediately?

Do I Have to Pay Capital Gains Taxes Immediately? In most cases, you must pay the capital gains tax after you sell an asset.

Do I pay taxes to the IRS when I sell my house?

If you do not qualify for the exclusion or choose not to take the exclusion, you may owe tax on the gain. Your gain is usually the difference between what you paid for your home and the sale amount. Use Selling Your Home (IRS Publication 523) to: Determine if you have a gain or loss on the sale of your home.

How long to own a house before selling to avoid capital gains?

The 121 home sale exclusion comes with specific restrictions: Eligibility: To be eligible for the exclusion, you must have owned and used the property as your primary residence for at least 2 of the 5 years preceding the sale.

How do you avoid capital gains tax on property?

A few options to legally avoid paying capital gains tax on investment property include buying your property with a retirement account, converting the property from an investment property to a primary residence, utilizing tax harvesting, and using Section 1031 of the IRS code for deferring taxes.

How do you calculate capital gains tax on the sale of a home?

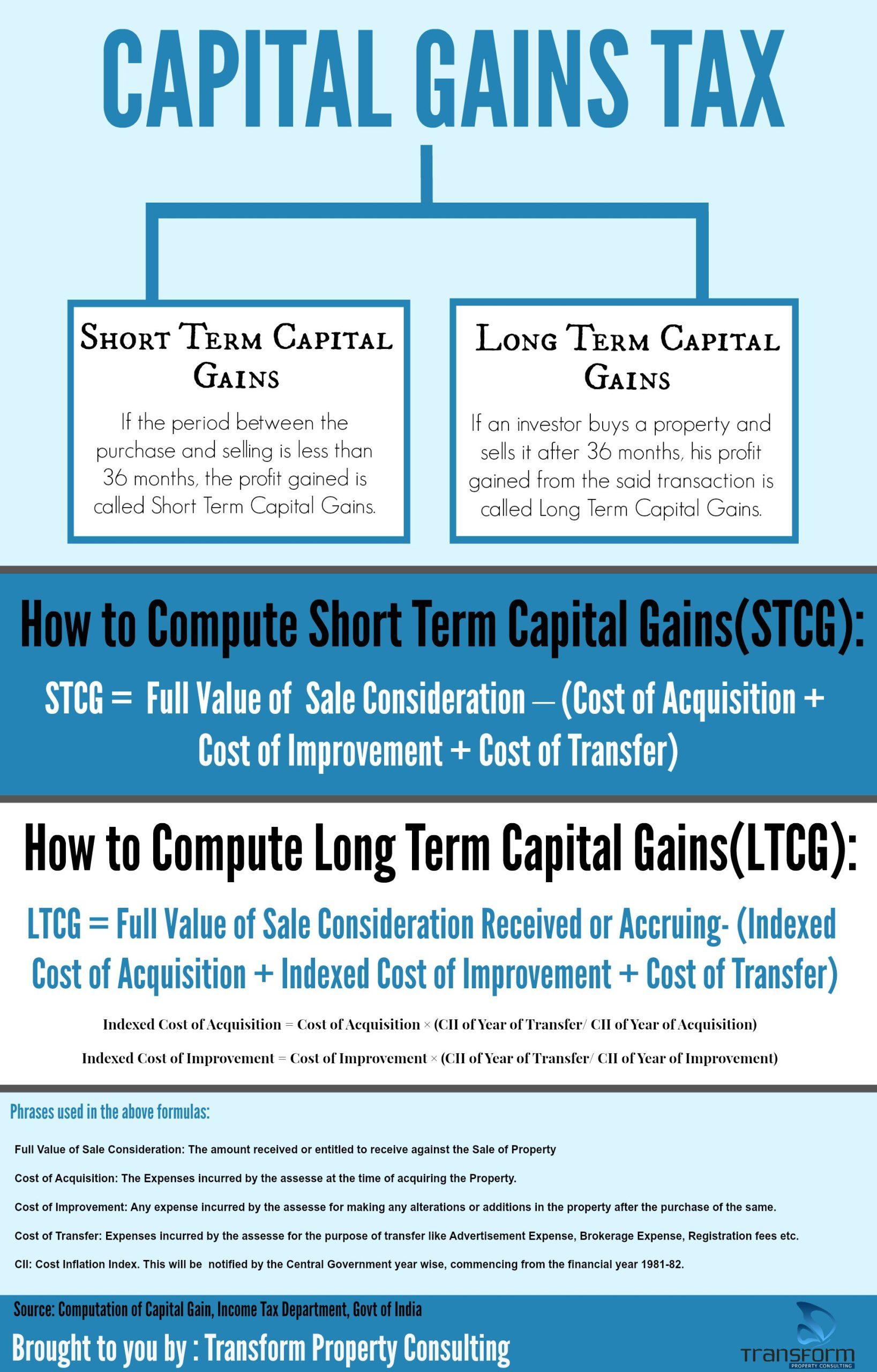

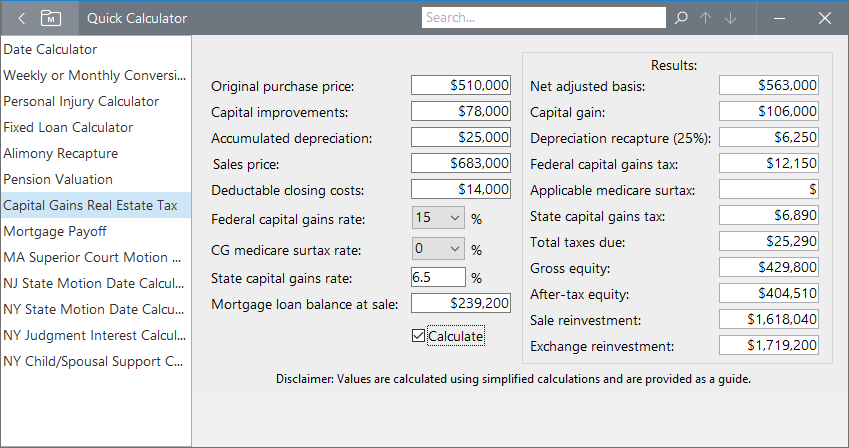

Capital gain calculation in four steps

- Determine your basis.

- Determine your realized amount.

- Subtract your basis (what you paid) from the realized amount (how much you sold it for) to determine the difference.

- Review the descriptions in the section below to know which tax rate may apply to your capital gains.

A common question we get is how do you calculate Capital Gains Tax, in the event that you’re the transferor of the property?

— KRA Care (@KRACare) January 18, 2023

Here’s a quick way to accurately do the math !

Read more here https://t.co/NwIpY9e0h0#CapitalGainsTax pic.twitter.com/Lkm3cmI04S

How much capital gains tax on $200,000?

= $

Jan 11, 2023

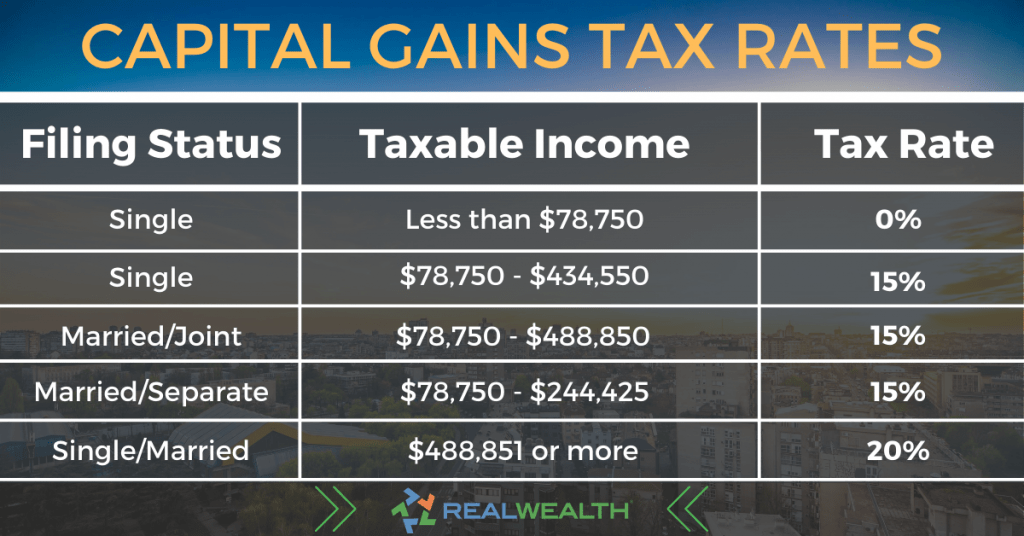

| Single Taxpayer | Married Filing Jointly | Capital Gain Tax Rate |

|---|---|---|

| $0 – $44,625 | $0 – $89,250 | 0% |

| $44,626 – $200,000 | $89,251 – $250,000 | 15% |

| $200,001 – $492,300 | $250,001 – $553,850 | 15% |

| $492,301+ | $553,851+ | 20% |

How much capital gains tax on $90,000?

A capital gains tax example

Your taxable income is $90,000 in the same year you sell your home, so your tax rate is 15%. You'll pay an estimated $7,500 in capital gains tax.

How do I avoid paying taxes on profit from selling a house?

Sale of your principal residence. We conform to the IRS rules and allow you to exclude, up to a certain amount, the gain you make on the sale of your home. You may take an exclusion if you owned and used the home for at least 2 out of 5 years. In addition, you may only have one home at a time.

How much profit can I make on my house without paying taxes?

You can sell your primary residence and be exempt from capital gains taxes on the first $250,000 if you are single and $500,000 if married filing jointly.

How much capital gains can I have without paying taxes?

Long-term capital gains tax rates for the 2022 tax year

| FILING STATUS | 0% RATE | 20% RATE |

|---|---|---|

| Single | Up to $41,675 | Over $459,750 |

| Married filing jointly | Up to $83,350 | Over $517,200 |

| Married filing separately | Up to $41,675 | Over $258,600 |

| Head of household | Up to $55,800 | Over $488,500 |

Does selling your primary residence count as income?

It depends on how long you owned and lived in the home before the sale and how much profit you made. If you owned and lived in the place for two of the five years before the sale, then up to $250,000 of profit is tax-free. If you are married and file a joint return, the tax-free amount doubles to $500,000.

How do I avoid capital gains on sale of primary residence?

Eligibility: To be eligible for the exclusion, you must have owned and used the property as your primary residence for at least 2 of the 5 years preceding the sale.

What are the tax consequences of the sale of primary residence?

You likely can exclude up to $250,000 of gain ($500,000 if married filing jointly) on the sale of your home. Some or all of the capital gains on the sale of your house are probably subject to capital gains tax. To be sure, check with a qualified tax professional.

Do you report sale of primary residence on Schedule D?

Per IRS Instructions for Schedule D, if you sold or exchanged your main home, do not report it on your tax return unless your gain exceeds your exclusion amount.

Does selling a house affect your tax return?

Any gain (profit) on the sale of your home may be subject to the capital gains tax. Your gain (or loss) is determined by subtracting your cost basis from your selling price, less selling expenses. A loss on the sale of your home is not deductible on your return.

How do I report gain on sale?

You'll have to file a Schedule D form if you realized any capital gains or losses from your investments in taxable accounts. That is, if you sold an asset in a taxable account, you'll need to file. Investments include stocks, ETFs, mutual funds, bonds, options, real estate, futures, cryptocurrency and more.

How do I report sale of home on Schedule D?

Home. If you have to report the sale or exchange, report it on Form 8949. If the gain or loss is short term, report it in Part I of Form 8949 with box C checked. If the gain or loss is long term, report it in Part II of Form 8949 with box F checked.

Is money from the sale of a house considered income?

You are required to include any gains that result from the sale of your home in your taxable income. But if the gain is from your primary home, you may exclude up to $250,000 from your income if you're a single filer or up to $500,000 if you're a married filing jointly provided you meet certain requirements.

Do I have to report the sale of my home to the IRS?

Report the sale or exchange of your main home on Form 8949, Sale and Other Dispositions of Capital Assets, if: You have a gain and do not qualify to exclude all of it, You have a gain and choose not to exclude it, or. You received a Form 1099-S.

Is there a way to avoid capital gains tax on the selling of a house?

The good news is that many people avoid paying capital gains tax on the sale of their primary home because of an IRS rule that lets you exclude a certain amount of the gain from your taxable income. Generally, people who qualify for the home sale capital gain exclusion can exclude: $250,000 of capital gains if single.

How much gain on sale of home is not taxable?

Key Takeaways. You can sell your primary residence and be exempt from capital gains taxes on the first $250,000 if you are single and $500,000 if married filing jointly.

How long do I have to buy another property to avoid capital gains?

Within 180 days

How Long Do I Have to Buy Another House to Avoid Capital Gains? You might be able to defer capital gains by buying another home. As long as you sell your first investment property and apply your profits to the purchase of a new investment property within 180 days, you can defer taxes.

What is the $250000 $500000 home sale exclusion?

There is an exclusion on capital gains up to $250,000, or $500,000 for married taxpayers, on the gain from the sale of your main home. That exclusion is available to all qualifying taxpayers—no matter your age—who have owned and lived in their home for two of the five years before the sale.

How do you beat capital gains tax on real estate?

How can I avoid capital gains taxes on real estate?

- Own and live in your house for at least two years before you sell.

- Sell before your profits exceed the allowable exclusion.

- Sell before you file for divorce: If you're planning to get divorced, you may want to sell your home first.

How do taxes change when you buy a house?

Mortgage interest is tax-deductible, and the advanced interest payment may be tax-deductible as well. If you recently refinanced your loan or received a home equity line of credit, you may also receive tax-deductible points over the life of that loan.

Should I include sale of home on taxes?

You generally need to report the sale of your home on your tax return if you received a Form 1099-S or if you do not meet the requirements for excluding the gain on the sale of your home. See: "Do I have to pay taxes on the profit I made selling my home?" above.

Do you pay sales tax when you buy a house in Indiana?

Generally, all sales of tangible personal property, including sales of construction material, are subject to Indiana sales tax, while sales of real property are not.

Do you pay sales tax when you buy a house in Florida?

We do not have sales tax on purchases of homes. We do have Documentary Stamp Tax, Intangible Tax, buyer pays for Owners Title Policy mostly. Plus of course you have your property taxes.

How much do you get back in taxes for mortgage?

In general, you can deduct the mortgage interest you paid during the tax year on the first $750,000 of your mortgage debt for your primary home or a second home. If you are married filing separately the limit drops to $375,000.

How much is capital gains on $100,000?

In this example, you see a capital gain of $100,000 on your home sale. If your income and asset class put you in the 20% capital gains tax bracket, you pay 20% of your profit. That's 20% of $100,000, or $20,000.

How do I calculate capital gains tax on sale of home?

Capital gain calculation in four steps

- Determine your basis.

- Determine your realized amount.

- Subtract your basis (what you paid) from the realized amount (how much you sold it for) to determine the difference.

- Review the descriptions in the section below to know which tax rate may apply to your capital gains.

What percent do you pay on the gain on sale of a house?

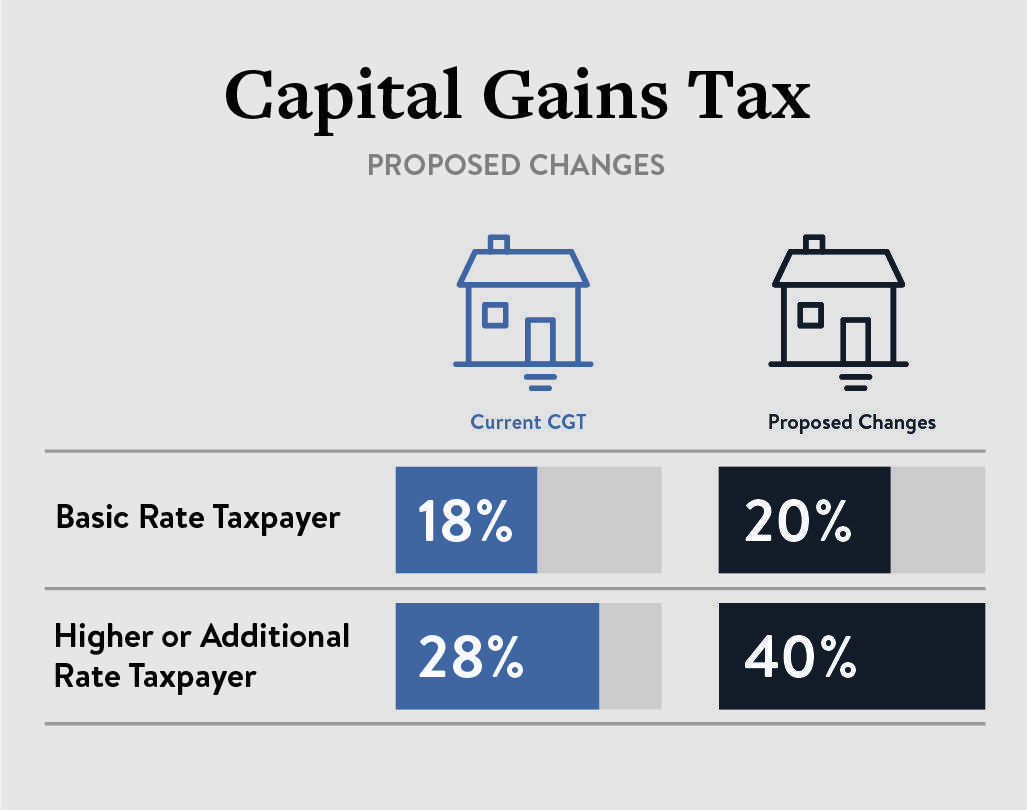

If you sell a house or property in one year or less after owning it, the short-term capital gains is taxed as ordinary income, which could be as high as 37 percent. Long-term capital gains for properties you owned for over a year are taxed at 0 percent, 15 percent or 20 percent depending on your income tax bracket.

Is there a 25% capital gains rate?

Capital Gains Tax Rate for Previously Deducted Depreciation

The rest of your long-term gain is taxed at either the 0%, 15% or 20% rate. For most people, this only comes up if you sell rental property. Once again, the 25% rate is a maximum rate.

How much does the IRS take when you sell a house?

Long-term capital gains tax rates typically apply if you owned the asset for more than a year. The rates are much less onerous; many people qualify for a 0% tax rate. Everybody else pays either 15% or 20%. It depends on your filing status and income.